The Business Case for Second-Party Audits

All types of organizations and operational processes demand a variety of audits and assessments to evaluate compliance with requirements—ranging from government regulations, to industry codes, to management system standards (e.g., ISO, GFSI), to internal obligations. Audits and assessments capture regulatory compliance status, management system conformance, supplier compliance, adequacy of internal controls, potential risks, and best practices.

Internal audits help identify problems so corrective/preventive actions can be put into place and then sustained and improved prior to third-party certification/compliance audits. Internal audits and assessments also help companies with continuous improvement initiatives.

Understanding the Internal Audit Process

Many organizations conduct internal audits with their own staff to assess conformance and identify opportunities for improvement. For companies large enough to have a dedicated internal audit team (with have no ties to the processes they audit), this may make perfect sense. However, it can take significant resources—time, personnel, money—to conduct all internal audits with internal resources.

It is easy to underestimate what goes into a successful audit and assume that it is more efficient and cost-effective to use internal resources. But that often isn’t the case. Let’s consider what an internal audit entails.

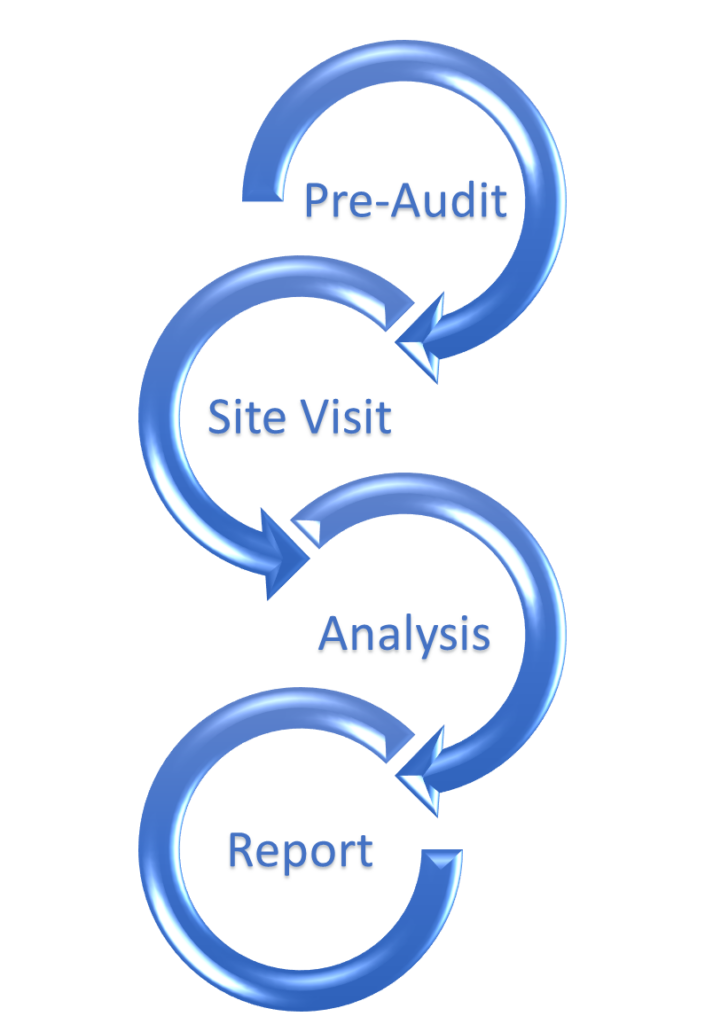

Pre-Audit Preparation

- Research: Auditors must understand the standard they are assessing against (i.e., regulatory, management systems, internal, industry). Effective auditors will also understand industry best practices; related local, state, and/or country-based requirements; processing norms for new product areas; etc. that can impact operational compliance and risks.

- Logistics: Logistics includes coordinating with the facility(ies) to schedule the audit and time with applicable personnel for interviews and, if travel is required, researching/booking flights, booking hotels, arranging for car transportation, etc.

- Document Review: Prior to the onsite audit, auditors should review available documentation (e.g., procedures, policies, programs). This will better inform and guide them on where they should dig more deeply during the audit, as well as help them create effective audit protocol (see below). Pre-audit document review also allows the onsite portion of the audit to remain focused on observing operations, interviewing workers, and verifying physical requirements are being met.

- Audit Protocol/Template: Auditors need to take the time to develop protocol/questions for conducting the audit, as well as standardized reporting templates, before the site visit. A standard protocol will make conducting multiple audits more efficient. Consistent protocols and templates also add value by allowing for direct year-over-year and site-to-site comparisons.

Onsite Audit

- Technical Knowledge: To efficiently conduct an audit, auditors must have a thorough understanding of the standard they are assessing against. In many cases, auditors are asked to juggle multiple areas of focus at once. For example, in a foods facility, the auditor may simultaneously evaluate Food and Drug Administration (FDA), U.S. Department of Agriculture (USDA), Global Food Safety Initiative (GFSI), and facility-specific procedure requirements. For an environmental, health, and safety (EHS) audit, the auditor may simultaneously assess Environmental Protection Agency (EPA), Occupational Safety and Health Administration (OSHA), state agency, and facility-specific requirements. Deep technical knowledge of all the related standards and codes helps to ensure a thorough audit.

- Audit Tools: Having the right tool for the job can make audits significantly more efficient. This includes the audit protocol and templates developed as part of pre-audit preparation, as well as audit tools that may be used to conduct and manage audits more efficiently and effectively.

- Audit Management: Auditors are responsible for building a relationship of trust and openness with the facility quickly, while still maintaining control of the audit. This can be a challenge for internal auditors when interviewing colleagues and assessing internal systems.

Post-Audit Follow-up

- Report: Auditors need to synthesize observations from the audit to create a report that concisely conveys all pertinent information, including nonconformances with the defined standard(s). Auditors provide additional value when they can leverage their industry experience to prioritize findings and identify opportunities for improvement and best practices. Reports are most valuable when finalized within a few weeks of the site visit when information is fresh to facility staff.

- Corrective Actions: After an internal audit, facility staff will inevitably have questions regarding findings and what to do next. Auditors can provide valuable support by offering recommendations, building corrective action plans, and supplying technical guidance.

Many organizations do not have dedicated internal auditors—rather, internal auditing is an “add-on” responsibility—so time spent completing these internal audit activities takes time away from other business responsibilities. This often results in a post-audit period where the internal auditor has significant catchup to complete other work that has been put on the backburner while conducting the internal audit.

Value of a Second-Party Auditor

A second-party auditor can provide an objective assessment of overall compliance status and, in many cases, do it more efficiently than organizations are able to do with their own resources. A second-party auditor has the time required to conduct the audit, travel, review documents, and create a report. Beyond that, a second-party auditor also has audit tools and templates to create efficiencies when conducting the audit and reporting, can consolidate audit trips, and can spend dedicated time completing all audit activities as efficiently as possible without needing to factor in other business responsibilities.

Beyond saving significant resources, using a second party to conduct audits provides significant business value and additional return on investment:

- Objectivity: Enlisting a qualified outside firm to conduct an audit provides a fresh set of unbiased eyes to assess aspects of your program internal staff may not consider or see. Second-party auditors offer broad perspective and knowledge of best management practices from conducting audits across industries and standards. They maintain ongoing, up-to-date awareness of current and pending regulatory requirements that the organization should consider.

- Customizable: The audits themselves can be customized to fit the needs and goals of the organization. A second-party auditor can provide more direct coverage to evaluate specific program effectiveness and allow for a more focused understanding of existing strengths and improvement areas. Whether there is a desire to prepare for unannounced regulatory agency visits, review plans and programs, assess supplier compliance, or even verify applicability, second-party audits can be built to address the organization’s identified concerns and help manage risks.

- Effective Tools: Second-party auditors often bring effective audit tools to help conduct and manage audits. These tools capture regulatory compliance status and certification system conformance more efficiently, track audit progress/completion status by subject, and generate reports that can be used by management to inform decision making.

- Efficiency: Audits performed internally can take resources away from normal business operations not only when conducting the audit, but also when catching up on daily responsibilities and work that is set aside during the audit. Second-party auditors work with the resources allocated to them to conduct an audit in a timely manner that does not negatively impact business functions. These audits minimize the overall disruption in business compared to internal audits.

- Validation: Second-party auditors validate existing programs and identify areas where best practices can be implemented to further protect the company. They assist in identifying and prioritizing issues before they become violations—focusing on implementing and closing corrective actions. They also provide data and reports that can be shared internally with employees to improve performance or externally with communities or customers to bolster the company’s image.

- Consistency: Using the same second-party auditor to conduct your audits creates consistency across locations and over time. This allows the organization to establish a benchmark for performance that can be used to help ensure continuous improvement throughout the organization and its supply chain.

Second-party audits are not just about checking boxes—they are about building stronger partnerships, spotting issues early, and keeping your business running smoothly. Don’t wait for nonconformances to catch you off guard. Implementing second-party audits isn’t just a compliance tool, it is a strategic advantage.

Comments: No Comments

Climate-Related Disclosures: SEC Final Rule

Agencies across the globe have implemented various voluntary and mandatory sustainability and carbon disclosure reporting requirements, ranging from the International Financial Reporting Standards (IFRS) Sustainability Disclosure Standards, to the EU Corporate Sustainability Reporting Directive, to the State of California’s climate disclosure legislation. Even the International Organization for Standardization (ISO) recently issued an amendment to ensure climate change impacts are considered by all organizations in their management system design and implementation.

On March 6, 2024, the U.S. Securities and Exchange Commission (SEC) followed suit, approving its much-anticipated final rule: The Enhancement and Standardization of Climate-Related Disclosures for Investors (Climate-Related Disclosure Rule). Initially proposed in March 2022, the SEC’s final rule requires publicly listed companies to report on greenhouse gas (GHG) emissions; climate-related risks; and other relevant environmental, sustainability, and governance (ESG) information. According to the SEC, the final rules are a continuation of the SEC’s efforts to respond to investor needs for more consistent, comparable, and reliable information about the financial effects of climate-related risks on a registrant’s business.

Overview of Requirements

The SEC’s recent action represents a significant milestone in the U.S., as it integrates climate-related risks and opportunities into business practices and investment decisions. Fundamentally, the final rule requires companies to:

- Identify any material climate-related risks, assess their impacts on financial performance and business strategy, and outline activities to mitigate or adapt to such risks.

- Disclose how they manage the oversight and governance of identified climate-related risk (i.e., the role of management and the Board of Directors).

- Provide information on any climate-related targets or goals that are material to the registrant’s business or financial condition.

- Provide comprehensive disclosure and attestation reporting on Scope 1 (i.e., direct) GHG emissions and Scope 2 (i.e., indirect) GHG emissions (large accelerated filers (LAF) and accelerated filers (AFs)).

- Disclose financial impacts of severe weather events and other natural conditions.

The final rule modifies the March 2022 proposed rule in several ways, most notably by removing the requirement for Scope 3 GHG emission disclosures and providing more time to implement disclosures and related assurance requirements. The SEC Fact Sheet provides a more comprehensive overview of all requirements included in the final rule.

The SEC Fact Sheet provides a more comprehensive overview of all requirements included in the final rule.

Timeline for Compliance

The final rule becomes effective 60 days after publication in the Federal Register. The requirements will be phased in for all registrants with the compliance date dependent upon the status of the registrant as an LAF, AF, or non-accelerated filer (NAF); smaller reporting company (SRC); or emerging growth company (EGC) and the content of the disclosure. Initial deadlines for Scope 1 and 2 GHG disclosures for LAFs begin as early as FY 2026. Refer to the SEC Fact Sheet for a breakdown on all deadlines.

What to Do

If it isn’t happening already, facilities need to start gathering emissions data, develop and implement a system to track GHG emissions, and create an action plan for climate disclosure. Even non-publicly traded companies can benefit from adhering to the general requirements of the new regulations, as publicly traded customers may require climate-related information. This presents an opportunity to demonstrate a commitment to ESG and improve brand reputation; an energy consumption analysis can also lead to improved efficiencies and cost savings.

For many, the SEC’s final rules have the potential to significantly expand requirements beyond what the company is already doing. The transition timeline is designed to allow companies the time needed to:

- Ensure the company has a robust management system in place to provide a solid framework for conducting the required risk assessments, managing new reporting requirements, and organizing required documentation. Note that ISO has taken recent steps to build climate change considerations into all its management system standards.

- Understand current disclosure reporting capabilities, data requirements, processes, and controls, then analyze what climate-related data has already been gathered and what additional information is needed to comply with the final rule.

- Establish or refine corporate governance and define clear roles, responsibilities, and charters for management oversight.

- Develop an action plan for implementation and integrate it with any other existing climate-related initiatives.

As organizations prepare to meet SEC disclosure requirements, KTL can help ensure they have the systems and processes in place to comply and to realize sustainable business value, including:

- Developing and implementing management systems that incorporate climate change considerations, including identifying environmental aspects and impacts, risks, and opportunities.

- Conducting energy audits and analyzing enterprise-wide energy consumption, trends, and opportunities for improvement.

- Calculating and tracking Scope 1, 2, and 3 GHG emissions.

- Identifying and planning for GHG emission reduction targets, renewable energy projects, and other opportunities to improve the organization’s carbon footprint.

- Developing information management tools to manage and track data and trend goals and objectives related to climate change.

FAQs on ISO’s New Climate Change Amendments

Effective February 23, 2024, the International Organization for Standardization (ISO) is integrating climate change considerations into all management system standards through its Climate Change Amendments. These Amendments ensure climate change impacts are considered by all organizations in their management system design and implementation.

ISO’s recent action supports the London Declaration on Climate Change of September 2021, which establishes ISO’s commitment to combatting climate change through its standards and publications. The aim of the recent Amendments is to make climate change an integral part of management systems design and implementation to help guide organizational strategy and policy.

What are the changes?

The Climate Change Amendments explicitly require climate change considerations in all existing and future ISO management systems standards, as incorporated into the Harmonized Structure (Appendix 2 of the Annex SL in the ISO/IEC Directives Part 1 Consolidated ISO Supplement). More specifically, the Amendments add the following two new statements to Annex SL for organizations to consider the effects of climate change on the management system’s ability to achieve its intended results:

- Clause 4.1: The organization shall determine whether climate change is a relevant issue, as it relates to understanding the organization and its context.

- Clause 4.2: NOTE: Relevant interested parties can have requirements related to climate change, pertaining to understanding the needs and expectations of interested parties.

The broad scope of these Amendments (i.e., impacting all standards) reflects ISO’s commitment to integrating climate considerations across diverse operational areas (e.g., environment, quality, safety, food safety, security, business continuity, etc.).

What do these changes require?

The original intent and requirements of Clauses 4.1 and 4.2 remain unchanged; however, the Amendments now require organizations to consider the relevance of climate change risks and impacts on the management system(s).

Potential climate change issues will likely differ for the various standards. The Amendments ensure these various risks are considered for each standard and, if actions are required, allow the organization to effectively plan for them in the management system.

What do certified organizations need to do?

Organizations that are certified—or are planning for certification—need to make sure they consider climate change aspects and risks in the development, maintenance, and effectiveness of their management system(s).

The Amendments specifically require these organizations to evaluate and determine whether climate change is a relevant issue within their management system(s). If the answer is yes, the organization then must consider climate change in a risk evaluation within the scope of their management systems. Where relevant, organizations are further encouraged to integrate climate change into their strategic objectives and risk mitigation efforts. The Amendments do not require organizations to do anything about climate change beyond considering the impacts on the management system’s ability to achieve its intended results.

What is the timeline?

The Amendments are effective as of the date of publication. There is no transition for implementation.

Certification bodies and auditors will cover the Amendments in audit activities when assessing this section of a management system. The audit will ensure climate change is considered and, if determined to be a relevant issue, included in company objectives and risk mitigation efforts. If climate change is deemed not relevant, the audit will assess the organization’s process for making this determination.

Will new certifications be issued?

Because the changes are considered a clarification, ISO issued them in the form of an amendment. New standards will not be republished until new versions are released; therefore, the publication year of each ISO standard will not change, and no new certifications will be issued.

What are the benefits of these changes?

The Climate Change Amendments underscore the importance of understanding and addressing the impacts of climate change. By publishing the Amendments in Annex SL, ISO is leveraging the widespread adoption of all ISO management system standards across operational areas to integrate environmental stewardship into organizational practices, promote sustainability, and drive climate change action on a global scale.

For certified organizations, the Amendments are intended to enhance organizational resilience and adaptability to climate-related risks. Considering climate change in this way can significantly contribute to business sustainability and long-term success by:

- Ensuring regulatory compliance (e.g., emission limits, sustainability reporting, etc.).

- Creating positive brand reputation as a sustainable company and associated customer loyalty.

- Managing risks and opportunities associated with supply chain disruptions, energy efficiency initiatives, employee health and safety, natural disasters, etc.

- Engaging employees and attracting new talent who prioritizes sustainability.

- Providing access to markets and investors that have sustainability requirements.

Comments: No Comments

What Is an Energy Audit–And Why You Should Do One

Want to reach your sustainability goals, improve your energy efficiency, and save money? An energy audit can help you better understand your energy usage and issues—and identify opportunities to create energy efficiencies, reduce your carbon footprint, and positively impact your stakeholders.

What Is an Energy Audit?

An energy audit is a key part of energy management. Energy management involves monitoring and controlling energy consumption across an organization to save energy, save money, and protect people and the environment. Energy management should be part of any organization’s overall strategy. An energy audit helps determine energy usage and opportunities for efficiency projects at your facility, building, or process. The overarching goal of an energy audit is ultimately to reduce energy consumption and improve efficiency without impacting work processes or products.

Types of Energy Audits

An energy audit can take a range of forms depending on how detailed and extensive it needs to be:

- Preliminary Analysis: Review bill, conduct energy usage trending.

- Treasure Hunt: Conduct a group exercise walking around identifying obvious wastes.

- General Audit: Analyze specific systems, conduct detailed inspection.

- Comprehensive Audit: In addition to the areas covered above, may include longer term monitoring and mechanical/electrical/civil engineering reviews.

- Ongoing Audit: Long-term monitoring of efficiency systems, scheduling retro-commissioning.

General Energy Audit Process

In general, the energy audit process comprises several steps and activities that culminate in final recommendations to improve energy performance and efficiency.

The pre-audit is a desktop review that helps to identify energy consumption patterns, including the energy “hogs” and peak usage trends (i.e., the hours of the day during which demand for electricity is the highest). It consists of the following activities:

- Review utility bill for demand charges, power usage, load factor.

- Demand charges are fees applied based on the highest amount of power drawn during any interval during the billing period. Demand charges can comprise a significant proportion of commercial customers’ bills.

- Load factor is a measure of the utilization rate or efficiency of electrical energy usage. It is an indicator of how efficiently energy is being utilized.

- Review equipment repair and occupant complaint logs.

- Review past audit results.

- Discuss with management internal goals, financial criteria, upgrades, and future plans.

The site visit allows the auditor to observe facility operations and assess how systems are operating in practice. It comprises activities such as the following:

- Conducting interviews with operators, key decision-makers, and other plant staff.

- Collecting data, including facility data, nameplate data, forms, and logs.

- Performing a site walkthrough/tour to review:

- Site development.

- Building envelope.

- BTUs of boiler/HVAC, compressors, refrigeration, large equipment, etc.

- Building exterior (e.g., roof plan, outdoor lighting, exterior equipment).

- Taking measurements (i.e., combustion, lighting, temperature, ultrasonic).

After collecting the pre-audit documentation and site visit observations, the auditor is able to then perform a detailed analysis of energy performance. This analysis involves calculating the following:

- Energy usage, including baseload and peak energy, adjusted for weather, occupancy, and production.

- Energy costs, including accurate application of rates, time of use applications, seasonal applications, utility bill ratchet.

- Energy efficiency measures (EEMs), including material and installation, disposal, engineering design, permits and fees, and rebates and incentives.

The final report provides an action plan highlighting short-term (i.e., low-hanging fruit) opportunities, long-term budgeted improvements, and company goals. It should also reference site management, potential future problems, and testing programs that can all impact energy programs and operations.

Impacting People, Planet, and Profit

Energy audits directly impact the three Ps of the triple bottom line:

People. The United Nations has identified climate change as the number one threat to human societies. Brown energy releases can substantially impact air quality and have significant negative impacts on human health. Creating energy efficiencies and reducing the use of non-renewable energy is key to mitigating this threat. Beyond the human health threat, improved EEMs can improve employee satisfaction and, subsequently, create a corporate culture shift that embraces sustainability. For example, optimized lighting, ventilation controls, and incentives for driving electric vehicles may lead to healthier and happier employees and improved retention.

Planet. In its simplest terms, reducing energy usage helps reduce carbon footprint and mitigate the impacts of global warming. For example:

- Fossil fuels are a finite resource. Reliance on them leads to the destruction of protected ecosystems and habitat. Lower energy demand decreases the need for power generation and the use of fossil fuels.

- Energy audits identify ways to reduce energy use. This, in turn, reduces air emissions and global pollution levels. The equation is simple: the less energy you use, the fewer carbon emissions you produce.

- Beyond energy efficiencies, energy audits also identify waste. Eliminating these waste streams prevents unnecessary landfill use and contributes to environmental sustainability.

Profit. The Carbon Trust estimates that most businesses can cut their energy costs by at least 10% (often by 20%) with simple actions that offer a quick return on investment. Operating more efficiently reduces energy consumption, which equates to significant savings on utility bills. This is particularly important as energy costs reach all-time highs. In addition, organizations that consume significant amounts of energy are at greater risk of being impacted by energy price increases or supply shortages. When an organization can reduce its demand for energy, it also reduces the risks associated with an energy shortage. Having greater control over energy consumption creates resiliency against energy price fluctuations.

Return on Investment

Once you have a comprehensive understanding of how energy is being consumed, it becomes possible to identify inefficiencies and opportunities for improvement, whether related to behavior (e.g., asking employees to turn off lights every night), technology (e.g., implementing integrated building management systems), or process (e.g., increasing operations during off-peak hours).

Energy audits may identify the following opportunities to reduce costs:

- Reducing operational inefficiencies, including continual running of motors, unoccupied spaces (light sensors), compressed air leaks, and others.

- Implementing EEMs, such as monitoring systems for malfunctions, insulating hot/cold water piping, implementing efficient lighting, and ensuring heat recovery.

- Optimizing building systems, including ventilation systems, lighting control systems, insulation, efficient windows, green roofs, etc.

- Identifying financial incentives, rebates, and demand response programs.

Energy Audit Best Practices

To get the most out of an energy audit, it takes time, data, budget, and buy-in. The following can help ensure your audit is successful and provides return on investment:

- Start small, plan ahead. Select the right type of audit based on the resources (i.e., time, financial, personnel) you have available. You can scale up your efforts over time.

- Set clear objectives. Identify what your organization wants to get out of the audit. Consider the 3 Ps—people, planet, and profit—and be open-minded. It may be about energy savings and cost reduction, but it also may be about meeting sustainability goals, creating a culture change, or retaining and attracting employees.

- Gather data. Review utility bills. Trend energy consumption. Assess building specifications.

- Enlist audit expertise. Engage the right auditors with the right qualifications. A Certified Energy Manager (CEM) and someone with an engineering background can add a depth of expertise to help identify concerns and opportunities beyond the “low-hanging fruit”.

- Conduct routine inspections and assessments. Update your maintenance program to include steam trap surveys, compressed air leak inspections, duct cleaning, and other routine inspections. These routine inspections allow for early detection of costly issues, and predictive maintenance can help reduce downtime and expand equipment life.

- Conduct routine measurement and verification. Just because you have implemented a system, process, or equipment does not mean that it is functioning as intended. Assess your EEMs regularly to ensure they are achieving the desired results.

- Engage your stakeholders. Include management staff, employees, and other decision-makers in your efforts. Engaging these stakeholders in creating solutions can help create buy-in and a culture change that makes energy efficiency and sustainability a way of doing business.